Kevin Slater

-

Posts

5,454 -

Joined

-

Last visited

-

Days Won

2

Kevin Slater's Achievements

")

-

Kevin Slater reacted to a post in a topic:

Roth Conversion - any regrets?

Kevin Slater reacted to a post in a topic:

Roth Conversion - any regrets?

-

Kevin Slater reacted to a post in a topic:

Roth Conversion - any regrets?

-

Kevin Slater reacted to a post in a topic:

Openly Gay Man To Sign US Currency

Kevin Slater reacted to a post in a topic:

Openly Gay Man To Sign US Currency

-

thomas reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

thomas reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

-

BSR reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

-

MikeBiDude reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

-

Reminder: this is a forum to discuss the markets and finance, not other posters.

Reminder: this is a forum to discuss the markets and finance, not other posters. -

Kevin Slater reacted to a post in a topic:

CD rates on the rise

-

+ nycman reacted to a post in a topic:

Credit card debt hits 1 trillion! How much do you owe?

+ nycman reacted to a post in a topic:

Credit card debt hits 1 trillion! How much do you owe?

-

I would find that very hard to believe. Kevin Slater

-

+ Vegas_Millennial reacted to a post in a topic:

Kiddo in NYC

-

+ Vegas_Millennial reacted to a post in a topic:

Kiddo in NYC

-

+ Vegas_Millennial reacted to a post in a topic:

Kiddo in NYC

-

+ Vegas_Millennial reacted to a post in a topic:

Kiddo in NYC

-

Kevin Slater reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

-

Kevin Slater reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

-

Every five to seven years, people forget that the Dow has a correction every five to seven years. Kevin Slater

-

Kevin Slater reacted to a post in a topic:

CD rates on the rise

-

Inflation continues to fall

Kevin Slater replied to EZEtoGRU's topic in Personal Finance & Investing

Inflation numbers will be suspect until we get a year away from the (previous) government shutdown. While the BLS wasn't collecting data throughout the shutdown, they simply assumed the same price as last time they checked. It'll take a full year for those acknowledged bad numbers exit the equation. Kevin Slater -

Kevin Slater reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

Kevin Slater reacted to a post in a topic:

How long till Dow Jones hits 40,000 and S&P 5,000?

-

There's a good argument to be made that gold is now just a meme stock. Kevin Slater

-

The formula is quite simple: a million more than you have today. Kevin Slater

-

I believe it's the converse, actually. Non-retirement (i.e. taxable brokerage) accounts get the stepped up cost basis (as of the date of death). Distributions from traditional pre-tax accounts are taxed to the beneficiary as ordinary income, regardless of what the investments were worth at death. For Roth accounts, there is no tax consequence. Kevin Slater

-

WBD Stock, Warner Brothers Discovery

Kevin Slater replied to TonyDown's topic in Personal Finance & Investing

I exited my position when the first deal was announced. Wish I had your dilemma instead. Kevin Slater -

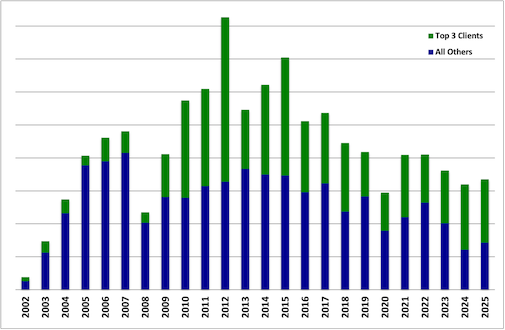

Looking at the chart, those top three clients. Kevin Slater

-

Per annual tradition: Revenue increased 6% in 2025. 57% of 2025 revenue came from the year’s top three clients, down from 62% in 2024. Last year’s top two clients retained their spots. As I’m only seeing a small number of repeat clients, revenue per client has more than tripled in the last three years. Kevin Slater

- 2 replies

-

- 16

-

-

-

What are they? I'll be happy to remember them for you. Kevin Slater

-

'No tax on tips' not for sex workers

Kevin Slater replied to Kevin Slater's topic in Personal Finance & Investing

And it's not clear how this will impact one's state taxes, depending on which state he lives in. Kevin Slater -

nytimes.com WWW.NYTIMES.COM Kevin Slater

-

Would you sign up for a 50-year mortgage?

Kevin Slater replied to marylander1940's topic in Personal Finance & Investing

That strikes me as the one upside: you basically are renting, but with a rent cap. After a while, that would be huge. Kevin Slater -

Yup, I believe that to be the case. If he wanted the socials tied to his work life, he can be the one to do it. Kevin Slater