bigjoey

-

Posts

13,368 -

Joined

-

Last visited

Content Type

Forums

Donations

News

Events

Gallery

Posts posted by bigjoey

-

-

I have not seen him in a number of years but he’s one of the best. Not just his good looks and great sexual skills but his positive attitude guarantee you a great time.

He’s very intelligent and uses his intellect to figure out how to please you. His goal is that you have a good time and you will.

-

Interesting video on inflation:

-

17 minutes ago, FrankR said:

You may find this interesting…

https://fortune.com/2023/07/05/jeremy-grantham-billionaire-investor-gmo-predicts-stock-crash/

And the problem is: we’ll have to wait and only looking back know if he is correct. However, I find it interesting that he hedges his bet. He does not say the market will crash. He puts his prediction in percentage terms.

At any given time, a normal investor is saying a stock price has peaked and is selling and another investor is buying because they think it will go up. 50% of the investors are wrong. (I say “normal investor” because there is always some “forced” selling due to death, divorce and debt).

Like buying Coke in 1998, the “smart”, short term investor was a seller and the wrong, short term investor was a buyer. At that moment, the outcome was unknown; now, decades later we know who was right.

-

8 hours ago, stevenkesslar said:

Well, again, yes and no.

Yes. You're right that if you bought Coke stock in 1980 and sold it today, it went from a split-adjusted price of $1 to about $60. Not bad. And you got dividends along the way, which as of now are about 3 % a year. As I said above, my calculation of Berkshire's annualized return of 38 % a year compounded from 1980 to 1998 was crude. Because I didn't even include dividends.

No. Coke is an excellent example of my point above. If you bought Coke for $44 in 1998, at a peak, it took about 15 years for the stock to simply be worth what you first bought it for. Again, there's dividends along the way. But that's a long dry run for Coke if you're simply counting on dividends.

If we are talking Buffet-level wealth, the other thing that has to be factored in is capital gains taxes. It certainly makes no sense to pay short term capital gains rates by gaming a stock like KO every year. In large part because there's no reason to sell a stock like Coke when the stock price keeps going up. On the other hand, if you'd owned it for a decade and you thought it was topping in 1998 it could make sense to pay long term capital gains and get out and invest in something else. You'd have had 15 year to try "something else" and you could still buy it back for the same price.

Stanley Druckenmiller is a good example of an alternative billionaire strategy. His idea is to jump from one asset type to another. If Coke ain't working for you, buy gold. He's made money every year.

I'm not arguing against Buffet. Quite the opposite. My best investments have all been buy and hold real estate. And that works nicely because of the leverage of using the bank's money on a mortgage paid by tenants to gain appreciation.

When I first started trading stocks in 2000 I got the wrong impression, precisely because of what I pointed out above. In January 2000 buying Coke or Procter & Gamble was a bad idea. You wanted to buy some worthless biotech or .com company and make 100 % in a month or so. For some strange reason, that didn't last long. So what I eventually figured out is that it's better to view stocks like little homes. The more expensive, like Apple, usually the better. Although Berkshire itself costs more than most people's homes.

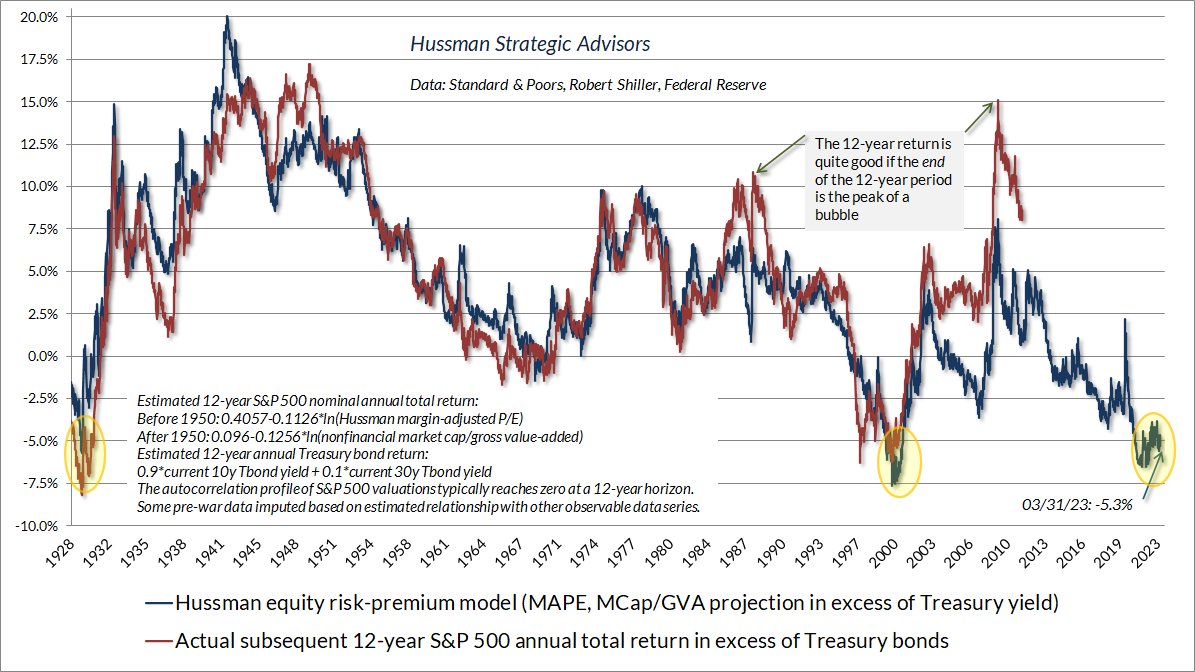

I posted that chart from John Hussman earlier in the thread. It's worth a repeat on this point of buy and hold. The debate I've been having with my nephew, who is skeptical about how long this bull market will last, is whether at some point it will just makes sense to buy Treasuries instead. The red line shows the annual return of the S & P 500 over Treasury bonds. Obviously, in most years going back a century it is better to invest in stocks rather than bonds.

Hussman is an excellent example of how to totally fuck up long-term investing. As I cited in a post above, he has been arguing since 2014 that the market is overvalued and it's time to get out. As his blue line "risk premium model" above shows. So he has the great distinction of being wrong and having crappy returns pretty much every year for a decade. I'd listen to Buffet instead.

The issue as I see it is if it is 1998 or 2000, and stocks like Intel or Coke, let alone Pets.com, having been going up like a skyrocket, maybe it is time to get out of a long term trade. And buy Treasuries, or something else. We now know that would have been a smart move in 2000. But by 2002 it was better to buy stocks again for years to come.

And in 2022, thanks to inflation, we also learned that even though it may have made sense to sell stocks and buy Treasuries, it turned out they both sucked. Basically, inflation sucks.

So, yes. It's always smartest to be like Buffet as Plan A. That said, I know my nephew is simply praying the rally lasts til Fall so he can cash out a 300 or 400 or 500 % gain, or whatever it is at that point, pay capital gains tax on a huge tech stock win at the long term rate, and try Plan B. Fucking Millennials! No patience. They always want it now.

The problem knowing that you shouldn’t have bought Coke in 1998 and that it would be 15 years before it reached that price level again is you are looking in a rear view mirror. While it’s obvious now, it wasn’t then. At any point in time with the knowledge of the time, decisions need to be made to buy and sell.

If you had bought Coke in 1998, looking at its past history, as it dropped the logical thought would have been that this is a temporary setback and will soon return to its upward path. When you take the very long term Buffett view of holding a dividend paying, quality company it seems to work (a long life helps, too). Market timing doesn’t work.

I agree with you about real estate. Normally, it’s a great long term investment.

One thing that needs to be considered: inflation. To accurately measure any investment return, the return needs to be inflation adjusted. Stocks, bonds and real estate returns to be accurate and to be compared over time must be inflation adjusted. A 10% return now and a 10% return during the high inflation Jimmy Carter years are different.

-

22 hours ago, stevenkesslar said:

Just out of curiosity, I checked. This relates to the point about whether aggregate economic factors, like inflation, really make a difference. Or whether what matters more is good value-based stock picking, like Buffet does.

And since you aced the first riddle, I'll try another.

Buffet and Charlie Munger decided to have a competition. Over a period of several years, Buffet bought stocks that increased in value at the rate of 38 % annualized. Munger did the same. Except his basket of stocks actually decreased about 2 % a year. Then Buffet let Munger in on a little secret. After that, Munger's next set of investments grew at the rate of 16 % a year. What do you think Warren's little secret is?

I read a very verbose and technical article years ago that argued that Warren Buffet is a secret market timer. And therein may lie the answer to the riddle.

Those numbers are correct. But it wasn't Buffet v. Munger. It was Buffet and Munger v. Time.

Berkshire Hathaway started around a low of $245 a share in 1980. By 1998, when it hit a peak, it was worth $84,000 a share. A crude calculation is that's about 38 % a year compounded.

From 1998 to 2009 Berkshire went from $84,000 a share to $70,000 a share. That's about a 2 % a year decline.

From 2009 to now Berkshire went from $70,000 to $543,000 and change. Crude calculation is that's about 16 % a year.

I'd argue it's not that timing is of the essence. It's that timing is the essence.

Of course, Buffet's point would still be that you can't predict these things. Like I argued, corporate profits actually grew way more in the Naughts than in the Nineties. And Buffet's portfolio is big and diverse enough that things like GDP and aggregate corporate profits and inflation matter. So since these things can't be predicted, just buy and hold, he says.

What's interesting that I just learned looking at the chart is that Berkshire Hathaway hit a peak in 1998. And then it actually hit a low in Spring 2000. Right when the Nasdaq was topping at 5000 thanks to companies like Pets.com. Another riddle. But that answer is simple: Coke. Buffet's beloved Coca Cola was worth about $1 in split-adjusted terms back when Berkshire got started in 1980. It peaked at $44 a share in 1998. By Spring 2000, when Pets.com was all the rage, Coke lost half its value and was selling for $22.

Coke is worth $60 today. If you bought it for $40 in 1998, you did okay. If you bought it for $20 in 2009, you did better.

Meanwhile, Pets.com hasn't been seen for a long time. Just like the imminent recession. 😉

Thoughts:

1- Buffett’s strategy includes stocks that pay huge dividends year after year: https://www.kiplinger.com/investing/stocks/best-warren-buffett-dividend-stocks#:~:text=And%20the%20best%20Warren%20Buffett,and%20%244.89%20billion%20in%202020.

Getting $6 billion in cash dividends adds value no matter what the market says Berkshire is worth. (At some point, after Buffett dies, I would expect the company to payout some of this largesse.)2-because many of the Buffett stocks are held decades and the dividends keep flowing, short term ups and downs in the market price of those stocks are not important. Think: Coke. As long as the dividend is “safe” year-to-year change in the stock’s price does not mean much.

Buffett holds stocks like HP whose growth potential is limited and the printer machine business declines BUT the ink business is a cash cow and adds to Berkshire’s cash pile💵💰. Instead of trying to “time the market,” the long term certainty has paid off well. Rather than try to run after short term gains with “hot,” flavor of the month stocks, slow and steady has done well.

3-looking at Berkshire’s stock between carefully selected time points is dangerous (and often can produce different results by changing the window) as well as looking in a rear view mirror. A better approach is to be “neutral” and use arbitrary “windows” like 5, 10, 15 or 20 to see how effective an asset holding strategy is.

For “seniors”: No matter what theory one uses for buying stocks, personally I believe it is best to be diversified among asset classes and even within any asset class. This will smooth out market ups and downs.

For example in the asset class of stocks, I hold mostly great dividend paying stocks but also I hold some stocks that don’t pay dividends but are stocks with a great, long term future (El Pollo Loco- a profitable restaurant chain that’s expanding nationally) or a solid record that produces long term capital gains (O Reilly Automotive).

-

On 8/10/2023 at 2:41 PM, stevenkesslar said:

So riddle me this, Batman.

Here's one that blew my mind when I learned it several years ago:

Buffet's argument is that it's not the economy, stupid. Except in the very long run. It's the profits of the strong companies you buy for cheap, and hold on to as they grow. As he has famously proven. Therefore, it follows that a period when corporate profits boom is great for stocks, right?

Nope. In the short term, it's not necessarily even the profits, stupid. From 1996 to 2000 corporate profits languished, from 587 billion in 1997 to 490 billion in 2000, as that FRED chart shows. Meanwhile the Nasdaq quadrupled, from 1250 to 5000 or so. Then from 2000 to 2006 corporate profits tripled, to almost $1.5 trillion. The Nasdaq went from 5000 to 2500 or so. When I first saw that years ago, I decided that's a riddle I can't figure out. Other than if you build a bubble on companies like Pets.com, that earn nothing, maybe it all makes sense.

More recently, the stock market behaved better. Corporate profits soared for a few years during COVID. So did the S & P 500.

Buffet himself diagnosed one of the problems in this 1999 essay. He pointed out that between 1964 and 1981 the US GDP rose 370 % and Fortune 500 revenues sextupled. During those 17 years, the Dow went from 874 to 875. The culprit? Buffet points to the precise subject of this thread: inflation. More specifically, sky high interest rates and things like 14 % 30 year Treasury bonds.

I think Buffet is right that is there is one consistent way to fuck up the stock market, it's the inflation, stupid. Pick any period when inflation stayed above 5 % for a year or more, and that's a stock bear market. From mid 1946 to end of 1947, pretty much the whole period from 1973 to 1992, and recently of course from late 2021 to end of 2022. They all sucked for stocks.

This still doesn't explain why the stock market went sideways in the Naughts. Even though inflation and interest rates were low and corporate profits soared. Slow digestion after we burped up a bubble, maybe? Sky highs PEs in the late 90's didn't help, either.

Thankfully, I read that essay decades ago and decided I can't compete with Buffet. So I'll just be a dumb whore, I figured. It worked out well for me. But when it comes to stocks, I figure it's best to be like Buffet. Apple is by far the biggest chunk of his portfolio. And it's the poster child for consistently growing profits and even a relatively consistent PE.

Anyhoo, now that COVIDflation is working its way out of the planet's digestion, hopefully it's clear skies ahead.

And, in deference to Buffet, I also think it's the PE, stupid. Apple went from a 20 year average PE of 25 to a forward PE of 32 today. A bit high. But nothing a little correction someday won't fix. Meanwhile, NVDA went from a 20 year average PE of 68 to a forward PE of 220. Talk about PE inflation! It's always fun while it lasts. But look out below.

The answer to the riddle is really easy.

The graphs and economic data you list are all aggregate data for an entire economy. No matter what the investment asset purchased (real estate, a bond, a stock), you are buying a singular investment asset and not the aggregate (unless buying an index fund).

For buying a specific asset, information about the general economy is interesting but not terribly relevant in making a decision on a specific asset.

Example: No matter the interest rate, inflation rate, GDP growth rate, unemployment rate, etc, a specific real estate piece’s value depends more on location, tenant, condition of building, length of lease, local and government policies, why the real estate is for sale, what purpose the buyer has in mind, etc. Aggregate factors in the general economy like interest rates will impact the value to some extent but other factors may over ride the aggregate ones.

The same with bonds and stocks. When the aggregate market is hitting new highs, there are usually a few stocks hitting new lows. When stocks in the aggregate market are hitting new lows, there are often a few hitting new highs.

The “art” of investing in real estate, bonds or stocks is focusing on a specific asset. Warren Buffett made his mark picking specific stocks and he often is buying when others are selling. He is often buying when aggregate factors are sending sell signals. He holds stocks for the long run and doesn’t sell when aggregate factors send sell signals that the market is going down.

Finally, no matter the theory one uses to buy, sell or hold investments, there is a luck factor. We need to acknowledge that no matter how skilled the investor is, luck plays a role.

- BSR, + stevenkesslar, + augustus and 1 other

-

2

2

-

1

1

-

1

1

-

Warren Buffett on economists buying stocks:

- + stevenkesslar and BSR

-

2

-

11 hours ago, tassojunior said:

TBH, in the American past many people were institutionalized for various bad reasons and motives. Revenge, powerful spouse, etc. And homosexuality was often top of the list. I guess the courts felt a need to establish a broad almost prohibition of institutionalization.

No reason there cannot be a moderate middle path between the two extremes and thoughtfully incarcerate those who need it.

-

-

On 11/8/2022 at 12:35 AM, augustus said:

@bigjoey is ok I believe. He liked a comment a couple of weeks ago.

I’m OK but rarely check-in anymore yet alone comment. It’s just not worth the effort and I have a very busy and full life outside the virtual world.

I just got tired of trying to defend myself from outright lies, distortions and slander by one verbose poster in particular. He is welcome to continue practicing his Saul Alinsky methods on others and perhaps fool many readers here. I will no longer play his games. It seems he views posting not as a discussion or exchange of ideas but a battle-to-the-death against anything opposing his very partisan beliefs.

I may occasionally post or like a comment but otherwise, I’ve got a real life and my time is too valuable to waste with nonsense.

-

I would hold off on crypto investment right now. From “The Economist” this morning:

The summer of crypto’s discontent

PHOTO: GETTY IMAGES On Wednesday, Iran will cut off electricity to its 118 authorised crypto-mining firms, hoping to relieve the country’s strained power network. It is a fitting move, as the mood darkens in the wider cryptoverse. The price of bitcoin fell nearly 15% on Saturday alone, triggering some $1bn in liquidation as traders who had borrowed money to make big bets failed to put up more collateral. Other crypto-coins tumbled too, although most have since recovered and the market appears to have stabilised. But bitcoin remains nearly 70% below its peak in November. That is wreaking havoc across the industry.

Lenders have suspended withdrawals, hedge funds have failed to meet margin calls and one exchange halted transactions altogether, fearing it might run out of funds. Even giant firms have been hit. Many—notably Coinbase—have announced layoffs of up to 20% of their workforces. This summer of discontent could evolve into a long winter for the fading stars of crypto.

-

On 4/27/2022 at 8:30 PM, handiacefailure said:

Museum of Sex and it's pretty small and only takes about an hour or so to go through.

The 9/11 museum and memorial for sure.

I like the Interprid. It's cool if you like space and air type museums.

One I really like that you never heard anything about is the Frick mansion

The Moma you can go through in a couple hours.

The Frick is an amazing place. Closed for a complete renovation of the house (new HVAC, opening part of the second floor). Currently, the collection is on display on Madison Avenue in the old Whitney. Interesting because you can see the collection in a different way than when it was in the house.

- Smokey, + WilliamM and handiacefailure

-

3

-

16 hours ago, OCClient said:

I doubt Buffet would buy anything right now that doesn't fit his value criteria.

So for the newbie investors, Buffet would remind to look for well run, good companies that are priced at an attractive value.I have watched investment TV shows that invite guests to talk about including crypto in your portfolio. I never agreed with that advice. However, if the newbies choose to branch out into crypto funds, always remember to diversify so that your nest egg is not consumed when one asset class collapses. A lot of guys where I work are into crypto. They talk about it a lot! I do worry about their stakes in crypto with the recent drop in value.

Is the crypto party over? Wonder what your co-workers are saying🤔.

https://www.cnn.com/2022/06/19/investing/bitcoin-price

-

5 hours ago, Kevin Slater said:

Depending on which individual stocks you have in mind, chances are they'd already be well represented in the broad-based index fund. Picking individual stocks can be a lot of fun, but to my mind that's a game you play after you have a firm foundation of index funds. I often tell the guys talk to about investing that they have "permission" to put 10% of their money into individual picks. That scratches the itch, and often ends up illustrating to them why putting 90% in broad-based funds was a good idea. You can't go wrong with low-fee index funds, like Fidelity Zero Total Market Index (FZROX, truly zero fee if done within a Fidelity account). In any case, make sure to look at the net expense ratio (basically, the rake they take to pay for administration). It oughtn't be greater than ~.5% ($5 for every $1000 invested, yearly), preferably less.

Kevin Slater

Agree but I would add the concept of “dollar cost averaging.”

-

12 minutes ago, EZEtoGRU said:

While interesting, this hardly sounds like advice for a newbie investor. Please be mindful of the topic at hand.

I feel the newbie investor can do this. I did after observation of some very wealthy real estate investors. God isn’t making any more land. My entire life, there has been inflation that has increased the value of most real estate that equals or exceeds rate of inflation. Inflation is the enemy of the middle class who does not own a home (first real estate investment).

-

1 hour ago, FrankR said:

Partnerships can be both a blessing and a curse. Partners get married and then you are also married to their crazy spouses…and later ex-spouses. And their high maintenance kids, each with an opinion. No thanks!

For a newbie with a little capital - Low cost, broad based index funds are the way to go, in my experience. Easy, tax efficient, liquid and flexible.

Absolutely correct. With little capital, investing in a low cost index fund should “beat the market” over the long haul. I would add fixed monthly investment amount to dollar cost average and not try to time the market. It requires discipline to dollar cost average but that will bring the best results.

-

37 minutes ago, OCClient said:

I doubt Buffet would buy anything right now that doesn't fit his value criteria.

So for the newbie investors, Buffet would remind to look for well run, good companies that are priced at an attractive value.I have watched investment TV shows that invite guests to talk about including crypto in your portfolio. I never agreed with that advice. However, if the newbies choose to branch out into crypto funds, always remember to diversify so that your nest egg is not consumed when one asset class collapses. A lot of guys where I work are into crypto. They talk about it a lot! I do worry about their stakes in crypto with the recent drop in value.

Bill Gates on crypto: https://amp.cnn.com/cnn/2022/06/15/tech/bill-gates-crypto-nfts-comments/index.html

Warren Buffett on crypto: https://www.cnbc.com/amp/2022/05/02/warren-buffett-wouldnt-spend-25-on-all-of-the-bitcoin-in-the-world.html

Mark Cuban (who was big on crypto and still SELECTIVELY believes in crypto: https://cointelegraph.com/news/mark-cuban-says-crypto-crash-highlights-warren-buffett-s-wisdom/amp

I am old enough to see all types of investment crazes. They do not end up well. Buffett believes in investing in companies that produce products or services; they rise and fall in value with how well they execute that role and how well those products and services are needed and used.

Even museum quality art and antiques go both up and down in value depending on changing tastes and fashions but at least it has some intrinsic value. To me, crypto seems to be valued solely on the greater fool theory: there will be a greater fool than I who will buy it from me for more than I paid..

-

45 minutes ago, FrankR said:

That is fair. I also doubt a newbie investor will have $200k for a down payment on a $1mil building.

The buildings I have bought have all been in a partnership with members of my family. There were five of us investors who each put in 20%. In my example, we would have each put in $40,000 which makes it fairly easy to start building real estate wealth. Also, that spread the risk as we could buy more properties over time.

-

8 minutes ago, The Big Guy said:

Not to oversimplify, but my advice is to learn from a recession business environment and apply it in future investment decisions and business cycles. I have found over 40 years of investing that I made more money by far from the decisions I made during bad times as opposed to the decisions I made during good times. In 2008 - 2010, I nervously chose to invest in stocks during a terrible recession and have been rewarded well over the Long Term. Good luck to all.

Warren Buffett would agree with you and over the last few weeks has been buying while stocks are “on sale.”👍

-

I lucked out and bought a policy that was so unprofitable for the insurance industry, policies with those terms are not longer being sold😇. I bought the policy in my 40’s and it was paid for in full after 10 years with no more payments. (I am now 76)

The policy only paid for long term care after I was 65. The actuarial calculation included the insurance company holding the money for at least 20 years with no payouts and for anyone who died, never paying out. The policy paid $300/day which covered costs thirty years ago; while it has a COLA factor, long term skilled nursing can run more. It does cover home aid instead of institutional care. It has no lifetime limit. It has a 60 day wait period before coverage starts once long term care is required (the actuarial calculation was that if you entered skilled nursing, you would not last long).

The policy predates the wide availability of “assisted living.” Back when I bought the policy there was only independent living and skilled nursing. As a volunteer, I was involved in Kansas City’s first assisted living facility about 25 years ago and it was a revolutionary concept and we did not know how people would accept it and if it would be fiscally viable. The actuarial calculation did not include such living arrangements.

In addition to all of the above, people are living longer (pre-Covid) and the insurance industry made the terms much less favorable on new policies.

-

9 hours ago, bigjoey said:

It depends on the property. I have a single user piece of property leased to a solid NYSE company. I had 80% down and the mortgage lender hardly seemed to care about my income or assets. The company had a 25 year lease (the lease ended last year and they renewed for another 20 years).

The lender looked at the strength of the tenant and joked with me at the time that it was like a bond. The location was a top location that they figured would only go up in value over time (it has).

A second trick with such a piece of property: when the first mortgage is paid off, take out a new mortgage. That money comes out TAX FREE😀. Do NOT spend that money but reinvest it in more similar properties. Rinse and repeat. This works when you are young and have a long investment window. It worked for me because I started early and am now 76😇.

Highly simplified example:

1-buy a $1 million dollar building . 20% down and $800,000 mortgage. It needs to be a building with a good tenant and a steady income stream.

2-once that mortgage is paid off, take out a new $800,000 mortgage. Your basis in the original building drops to $200,000 (for purposes of the example, let’s omit effects of depreciation on basis). Do not spend the money on personal items but reinvest it. Buy four new $1 million buildings with 20% down. You now own five $1 million dollar buildings. Rinse and repeat.

3-depreciation has sheltered some of your income from rent and gives you a higher after tax return on your investment.

4-the downside is after the second or third mortgage, the building will have a negative basis. IF you sell the building, that gives you a huge gain. HOWEVER, their are alternatives to selling so that money you got with each mortgage remains TAX FREE: 1031 exchange, donate to charity, never sell the building and your heirs get a stepped up basis.

5-this works if you are disciplined and reinvest the money and not spend it for personal needs. It is taking a long term view to build wealth. Luck is involved as your tenants need to be strong financially with long term leases and the sites need to be good ones and the leases triple net leases (tenants pay all the expenses).

A separate issue that I did NOT do because my properties were all triple net leases, is putting personal expenses onto the rental property. If you own rental property and manage it yourself: when you are putting in a new parking lot, the contractor puts in a new driveway at your home; when you put in landscaping at the rental property, landscape your own house; appliances, carpet, painting and repairs can all be written off on the rental property as business expenses. I am NOT advising or advocating this but just note it is often done. I list this as an observation only.😇

-

Just now, Kevin Slater said:

That has not been my experience. They want to be sure all all counts, including their perception of your ability to pay.

Kevin Slater

It depends on the property. I have a single user piece of property leased to a solid NYSE company. I had 80% down and the mortgage lender hardly seemed to care about my income or assets. The company had a 25 year lease (the lease ended last year and they renewed for another 20 years).

The lender looked at the strength of the tenant and joked with me at the time that it was like a bond. The location was a top location that they figured would only go up in value over time (it has).

-

On 6/16/2022 at 1:47 PM, keroscenefire said:

Thanks for this excellent advice. Real estate is going to be a bit tricky for me for the time being. Both because Denver is a crazy market and because with my new business I actually don't have a lot of monthly income on paper, which would make it very hard to get a mortgage. But as it grows, I expect to be able to show that I have the income necessary for a loan. That may still be 3-4 years away though.

The mortgage lender looks more at the value of the property and how much down you are doing. The larger the amount down, the safer the loan and less dependent on your personal sssets and income.

Going the REIT way, your income/assets make no difference.

-

11 hours ago, Kevin Slater said:

This presents a wonderful opportunity to deploy some of that cash.

How am I feeling? Like I've seen this before, and I know how it ends. It ends well.

Kevin Slater

Like you, I see this as a “buying opportunity.” Warren Buffet has been buying this week. It may not be the bottom but there are selective “good” buys. I have made some purchases. Like Disney, this may not be the bottom but over the long run, it’ll be OK.

This has been my stock buying pattern for over 50 years. My problem is that at 76, the “long run” is not so long🥲.

Don't Frette

in The Lounge

Posted

A company name.

Great products. They have a “hotel line” sold to top hotels. Great quality at a reduced price. The wife of a friend was a rep for that line and I bought my sheets through her.

Highly recommended🥇🏆